Inside the Steinhoff saga, one of the biggest cases of corporate fraud in South African business history – what lessons can we learn?

The darling of the JSE is now a pariah fighting for its life

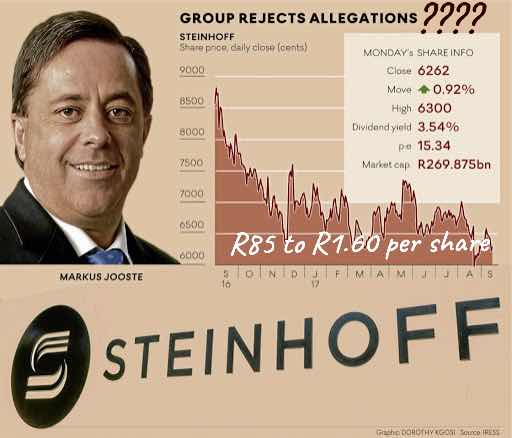

A capitalisation of 25b in May 2017 (R50 per share to 3b in May 2018 (R1.60 per Share at May 2018 with a questionable future)

A Spree of worldwide acquisitions and dodgy accounting and reporting – in the name of growth – made a house of cards come crashing down!

There are painful ramifications of the company’s reputational loss on friends, employees, pensioners and families; not to mention the misery caused to people around the world by the swift financial decline and uncertain future of this once-revered global retail giant.

The Steinhoff Story

- 1963 – Bruno Steinhoff – a furniture trader in Germany – entrepreneur selling household goods

- 1973 40m and 105 people

- 1983 230m and 320 people

- 1983 -1990 – Investment in Systems and warehouses

- 1993 600m and 3000 people

- 2016 8.6b with a reporter profit of 1.5b and 130,000 people

- 2017 Fraud found, dodgy accounting, lack of transparency , CEO resigns

“The Steinhoff group is an integrated lifestyle supplier that manufactures, markets, warehouses and distributes household goods and timber-related products.”

(Bruno Steinhoff, founder of Steinhoff International)“We have warehouses, we have distribution centres, we have logistics companies, we have retail stores, we have furniture production companies; we have the entire supply chain built up in all these countries.”

(Angela Krüger-Steinhoff, member of the Supervisory Board of Steinhoff International)

1994 – 2013 – South African Expansion

The paths of Bruno Steinhoff and Markus Jooste would cross when Steinhoff made a South African acquisition in 1997.

Through an m & a transaction in 1998 , Steinhoff International Holdings listed on the Johannesburg Stock Exchange and went on a major acquisition trail becoming a dominant player in South Africa.

A focussed acquisition strategy enables the company to grow to 87 factories and 26 distribution and sourcing locations, and operated in 10 countries.

It was now a fully vertically integrated furniture and household goods business with activities straddling manufacturing, sourcing and logistics. However, its retail operations were limited.

2014-2017 Acquisitions at any cost!

The vertical integration strategy required the development of retail activities across all the businesses in the group to fully control every aspect of the supply chain.

This, said Jooste, was the era of a breath-taking acquisition drive….. bolting on retail to its low cost supply chain!

Reporting showed massive profits from acquisitions that were purchased at massive premiums. growth at all costs!

Steinhoff was the darling of the investment community with the share price rocketing, while struggling retailers in the furniture world thought that all their christmases has come at once. A Win Win!!! Or was it????

Steinhoff operated in the following business categories:

1 Decoration

2 Furniture

3 Consumer electronics and cellular

4 Kitchen, bathroom and quick-fix essentials

5 Kitchens and appliances

6 Clothing and footwear

7 Beds and mattresses

Its brands have become truly global:

UK:

• Harveys (household goods)

• Bensons for Beds (household goods)

• Poundland (general merchandise)

• Pep & Co. (general merchandise)

• GHM! (general merchandise)

• Europe:

• Poco (household goods)

• Conforama (household goods)

• kika-Leiner (household goods)

• Pepco (general merchandise)

Africa:

• PEP (general merchandise)

• Ackermans (general merchandise)

• Russells (household goods)

• Incredible Connection (household goods)

• Unitrans (auto)

Australia and New Zealand

• Freedom (household goods)

• Best & Less (general merchandise)

• Harris Scarfe (general merchandise)

• Snooze (household goods)

As a result, the company has often been referred to as the “IKEA of Africa

In Dec 2017 – a huge fraud uncovered

Many of those acquisitions were not profitable, there were dodgy accounting practices and irregularities were uncovered!

The foundation could not sustain the house of cards that was to come tumbling down

Corruption is often justified on the grounds that it supports higher-order ideals, such as growing the organisation to become more profitable and sustainable and create more jobs.

However, organisational ideals and the pursuit of apparently worthy causes can inflate narcissism, offering management a level of protection against reality. As a result managers may start to believe that accepted norms can or should be sacrificed to attain higher-order values.

For example, when paying a bribe to a public official to secure a contract, or hiding losses or inflating profits on paper, the rationalisations might be: “I’m growing the company”, “I’m protecting shareholder value in line with my mandate” and “I’m protecting jobs”.

Those who have a utilitarian mind-set can easily be persuaded that the end justifies the means.

What are the psychological drivers behind and effects of unethical or illegal business behaviour.

What happened at Steinhoff could happen at any number of institutions.

Human morality is fragile, notwithstanding most people’s good intentions. Unconscious processes regularly lead individuals to engage in ethically questionable behaviours which are inconsistent with their visible characters and inherent beliefs.

Human beings are conflicted ‒ capable of great integrity and kindness, but also prone to envy and temptation.

There is no getting away from the fact that everyone embodies a mixture of good and bad. Freud described this relentless internal conflict between good and bad as the “tragic fate of humanity”, with fallibility being a normal part of the human experience.

Let us therefore not judge Steinhoff and Jooste from atop a moral pedestal, confident in the belief that this could never happen to us or our organisation.

Even the most moral of intentions can be undermined by an unconscious counter-will, which then triggers a moral collapse.

We cannot ignore the fact that there are potential Steinhoffs and Joostes in every corner of society.

WHAT BUSINESS LESSONS CAN BE LEARNT FROM THE STEINHOFF CASE?

The Steinhoff debacle – provide some important business lessons for small entrepreneurial concerns and large corporates alike.

- Lesson #1:

Be true to your strategic vision and ‘stick to the knitting’

Steinhoff did this exceptionally well

There is a case of deepening one’s competitive position and focus on your vision than going too broad and trying to be all things to everyone.

Steinhoff’s long-term vision has always been to control the value chain, thereby moderating costs, keeping competitors at bay and striving for ever-higher levels of efficiency and market share. Source and manufacture goods in low-cost countries and selling them to value-conscious buyers in more lucrative markets.

This vertical integration approach Steinhoff effectively ‘owns the neighbourhood’.

- Lesson #2:

Growth does not alway equate to profit or success – growth often means “cash burn”

Organisations that deliver consistently strong performance over extended periods of time invariably practise a controlled growth strategy in which future expansion and investments are carefully planned and executed.

The hallmark of truly great companies is that they have the discipline to hold back and moderate their growth plans so as not to experience resource constraints and fatigue, or end up in financial difficulties during lean times when the cash they accumulated during bumper years is all but exhausted.

Steinhoff’s extremely rapid acquisition drive, particularly in more recent years, was clearly unsustainable.

The nature of its investments (large, new regions and new product lines) signalled a high-risk approach which should have raised more questions from shareholders and the board about the company’s ability to sustain all the new acquisitions and ensure their profitability.

Growth invariably leads to cash burn

Such was the case with Steinhoff whose frenetic investment activity concealed highly complex business structures, high levels of debt and less-than-stellar performance within the Steinhoff group.

The management team, and Markus Jooste in particular, painted a picture of a fast-growing and practically invincible corporate giant which was too good to be true, and this should have set off alarm bells among different stakeholder groups.

- Lesson #3:

Strong governance is not just about financial and regulatory compliance; it is a mind-set

Most organisations extol the virtues of strong governance, as evidenced in prudent financial management, transparent reporting, and an engaged and accountable executive team and board.

However, all too often compliance ends up being a box-ticking exercise, with the goal being to meet minimum standards only ‒ i.e. simply to satisfy the relevant authorities.

Basic compliance may satisfy shareholders on a superficial level but it can lead to operational mediocrity if it is not backed up by enthusiastic and committed management, which is key to sustainable profits and a satisfactory return on investment.

An important dimension of sound management is a commitment to ethical business practices which are based on values, not just rules.

Values are deeply entrenched and highly personal belief systems which help people to distinguish between right and wrong and which therefore regulate their behaviour.

Rules provide behavioural guidelines but are susceptible to being challenged, manipulated or ignored.

As my mentor Allen Pathmarajah – a leader does the right things – a manager does “things right”

At Steinhoff, weak accountability and a culture of highly creative accounting meant that many dubious investment deals, excessive debt levels and the poor financial performance of several of the businesses went undetected for a long time.

Either the truth was hidden, or responsible parties (including the board) were not paying enough attention, or both.

Strong governance in an organisation is heavily dependent on an accountable and capable board to exercise rigorous oversight while also motivating the executive team to follow their vision.

It is a sad indictment of the corporate sector in South Africa that a company like Steinhoff was able to perpetuate the myth of unprecedented financial success for so long.

It is difficult to see how the company, given the magnitude of its financial problems and the scale of the deception, will survive in its current form.

When stakeholders, and especially investors, are betrayed, trust is rarely recovered.

- Lesson #4:

A charismatic leader can either be very good or very bad for a company

Many people believe that if an organisation is fortunate enough to have a charismatic leader, its chances of success improve dramatically.

Charismatic leaders have the ability to engage people at all levels, speak their language, keep their attention and earn their respect, which is no mean feat in an age when authority is regularly questioned.

Yet charismatic leaders are not always brimming with charm and goodwill. They can also be mesmerising in a frightening sort of way, extorting cooperation and loyalty through fear and charm.

The world has seen many brutal dictators keep their populations under control by projecting a charisma that is heavily laced with menace. Charismatic leadership is often viewed as ambiguous because the extraordinary power and influence that go with it can be used in either a positive or a destructive way.

Markus Jooste was clearly a charismatic leader who developed a strong and devoted following both within the company and across his many business and social networks.

Gregarious and generous to his inner circle, Jooste was afforded almost god-like status by his friends and close associates because to them he was a commercial superstar who had reached the pinnacle of professional and personal success.

However, he appeared to operate in the rarefied environment of the super-rich and super-successful who often believe themselves to be above the law.

While in one sense Jooste was the architect of Steinhoff’s runaway success in recent decades, from which scores of people benefitted in many different countries, he was also the main figure in the company’s recent fall from grace.

Driven by his own self-confidence, entrepreneurial talents and adulation from people around him, Jooste became a larger-than-life CEO who took great liberties with Steinhoff’s money and seemingly crossed all sorts of ethical boundaries.

Ultimately, this proved to be unsustainable.

Interestingly, many of his colleagues at Steinhoff – perhaps mesmerised by his superstar status – appeared to turn a blind eye to or were complicit in the large-scale “accounting irregularities” that were exposed in 2017, the news of which sent the Steinhoff share price into a tailspin.

This is an indication of how easily many people got caught up, knowingly or unknowingly, in Jooste’s seemingly unethical business dealings and ongoing deception about the health of the company. Even when Jooste resigned as CEO, his strangely chirpy email to the staff seemed to suggest that he deserved a slap on the wrist for leading people astray, which was a weak response in the face of such a grave turn of events.

- Lesson #5:

Even ethical business people are corruptible

Human morality is fragile, notwithstanding most people’s good intentions. Deep-seated stirrings of envy, greed, self-absorption, arrogance or a sense of entitlement could infiltrate people’s moral fibre at any stage – even those who appear to have strong value systems and are the least likely to be swayed.

To be human is to have to continually wrestle with one’s conscience when presented with opportunities to win friends, favours or influence without putting in the usual slog. It is, as Freud described it, a “tragic fate of humanity”.

Of course, this does not mean that wrongdoing should simply be pardoned – particularly when, in an organisational sense, the culpable parties are savvy enough or senior enough to know better.

What it does mean is that no organisation can afford to skimp on introducing the appropriate checks and balances, particularly where organisational finances are at stake.

- A final word

As renowned management expert, Peter Drucker, once said:

|

“Asking ‘What is right for the enterprise?’ does not guarantee that the right decisions will be made. Even the most brilliant executive is human and thus prone to mistakes and prejudices. But failure to ask the question virtually guarantees the wrong decision.” |

The Steinhoff story illustrates that business success can be attributed to numerous factors – from well-thought-out marketing and financial strategies and efficient production plants, to clear compliance guidelines and financial reporting standards. While efficient infrastructure and various management and operational tools are naturally important, the human factor stands out as being the most critical of all … and the most difficult to get right.

It is largely the human element that has toppled this once-mighty company.

- Compromised core values

- Lack of Transparency and Trust

- Growth at all costs – for the benefit of the greater good – “playing God”

- Charismatic leaders who lose their moral compass

Questions to be asked?

If there is a risk of significant financial loss occurring owing to unsavoury or unethical business practices, how might this risk be averted?

What can the Steinhoff story teach us in this regard?

Authors from Original Article

- Piet Naudé (Editor) is Director of the University of Stellenbosch Business School.

- Brett Hamilton holds an MBA from the University of Stellenbosch Business School where he is a visiting lecturer in Corporate Finance.

- Marius Ungerer is Professor of Strategy at the University of Stellenbosch Business School.

- Daniel Malan is Associate Professor of Corporate Governance and Head of the Centre for Corporate Governance in Africa, based at the University of Stellenbosch Business School.

- Mias de Klerk is Professor of Leadership and Human Capital Development, and Head of Research at the University of Stellenbosch Business School.