Jobkeeper Payments

With enrolment now open for the Federal Government’s JobKeeper program, here are the steps you can take to obtain the JobKeeper payment for their business.

1. Determine if you are an eligible employer

- Basic turnover test – for simple cases we need to verify that the relevant employment entity has faced a 30% fall in GST turnover, or is projected to have a fall in GST turnover compared to the same period last year.

- You can compare a month with the corresponding month last year (e.g. March 2020 with March 2019); or

- You can compare a quarter with the corresponding quarter last year (e.g. June 2020 quarter with June 2019 quarter).

- Once eligibility has been established, ongoing eligibility continues and testing is not required for future periods. However, there will be ongoing monthly reporting requirements.

2. Determine employee eligibility

- Employment must have commenced by 1 March 2020, and be currently employed either on a part or full-time basis, or have been a casual employee for more than 12 months.

- The employee must be notified of your intent to nominate them for JobKeeper, and they need to agree to the nomination by completing the JobKeeper employee nomination notice.

- You must keep a copy of that notice for your records. Whilst this does not need to be provided to the ATO there is a legal obligation to have it before claiming the JobKeeper payment for that employee.

You can access the required form here.

3. Ensure correct payment of eligible employees – payment will not be made if these steps are not met

- As the JobKeeper payments are made to you in arrears, payment of your employees must be made, in accordance with your ordinary payment cycle, before a claim can be made.

- A minimum of $1,500 before tax must be paid to each eligible employee each fortnight (or the equivalent thereof in your ordinary pay cycle) to be able to claim that fortnight. This is the case even if the employee ordinarily earns less than $1,500 per fortnight, with a top up amount being required for eligibility, and in advance of receiving the reimbursement.

- The one exception to the timing of payments is for the first two fortnights of 30 March 2020 to 12 April 2020 and 13 April 2020 to 26 April 2020. The difference can be paid late and eligibility will be retained provided a total of $3,000 for the two fortnights is paid to eligible employees by 30 April 2020.

4. Enrol in the program – Enrolment must be completed by 30 April 2020 to qualify for the April payment

Enrolment opened on 20 April 2020 and continues until 31 May 2020.

For enrolment you will need to provide:

• Bank details;

• Confirmation of entitlement to participate; and

• Confirmation of the number of employees who are entitled to receive the payment.

Enrolment can be completed either via the Business Portal or via your tax agent.

5. Apply for the program – commences 4 May 2020

- Application for the program commences on 4 May 2020 and continues until 31 May 2020 via the portal.

- Application involves selecting eligible employee details from submitted Single Touch Payroll (STP) lodgements completed through your payroll system and submitting this information to the ATO. If you do not know if your payroll system is STP compliant, or if you are unsure if STP lodgements are being made, please contact us to discuss.

- At this stage it appears that the STP information and indication of eligible employees may be required for lodgement each month.

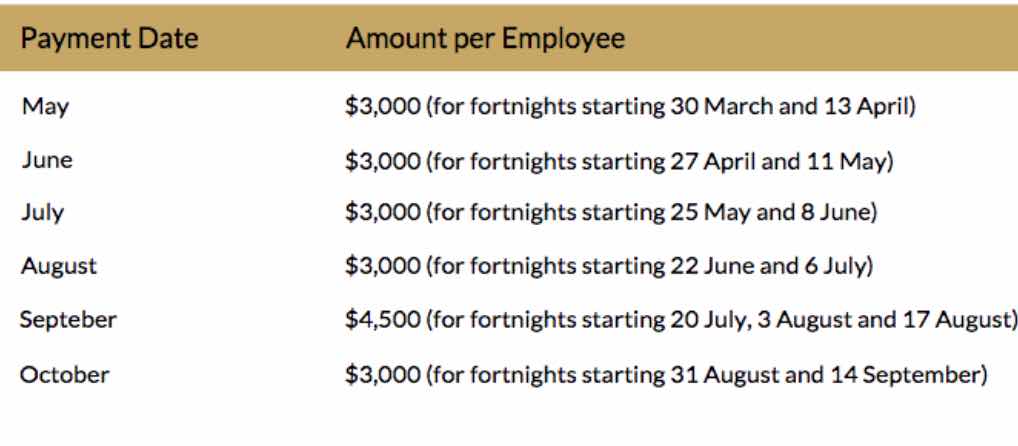

6. Timing of reimbursements

JobKeeper payments are a reimbursement, and cannot be made in advance. The table below outlines the timing of the reimbursements, and to which fortnights they relate to: